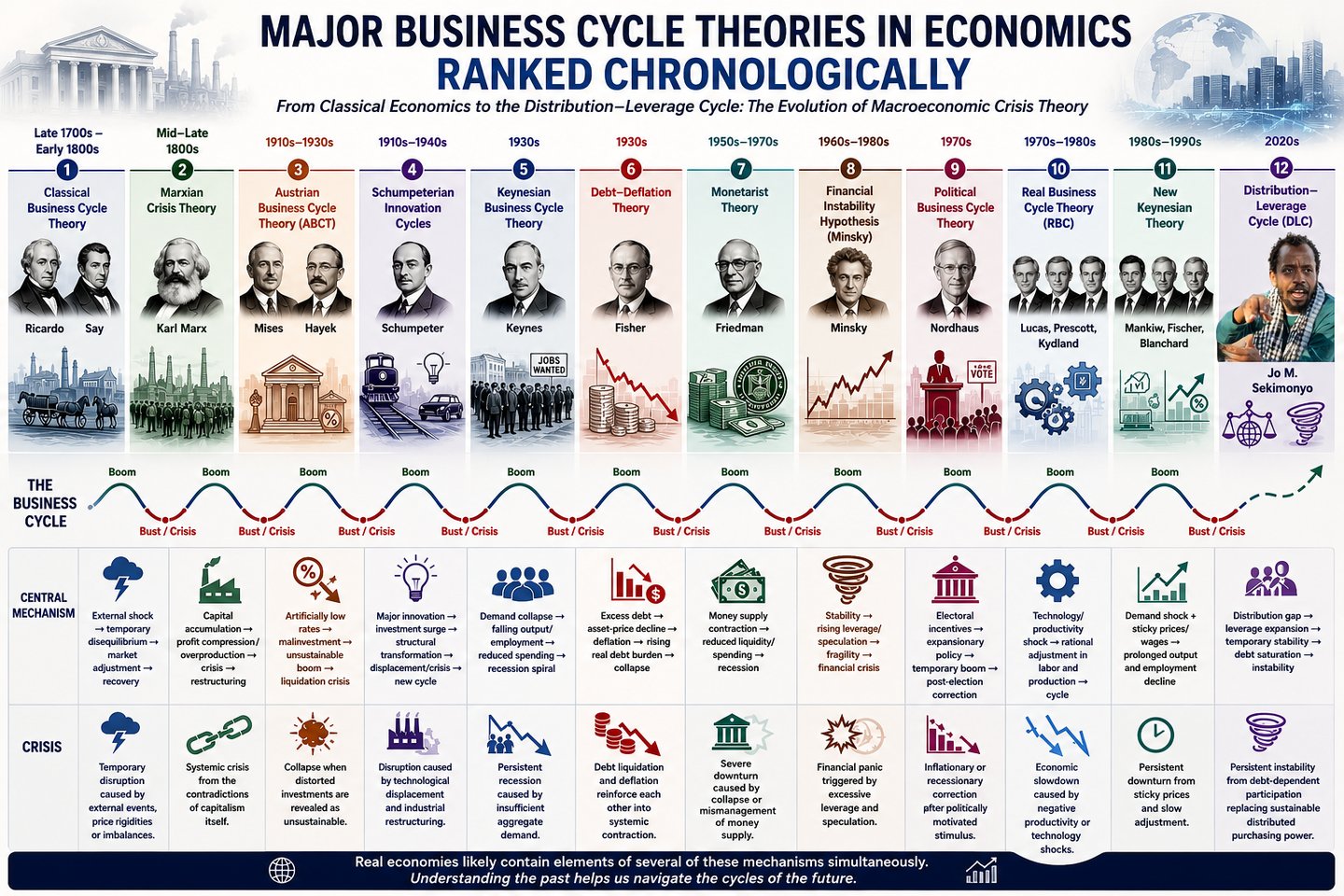

Major Business Cycle Theories in Economics Ranked Chronologically

Jo M. Sekimonyo

3/9/2026

There are many business cycle theories in economics, each trying to explain why economies experience booms, recessions, crises, and recoveries. They differ mainly on:

what causes instability,

whether markets self-correct,

and what role money, debt, technology, distribution, or institutions play.

1. Classical Business Cycle Theory (Late 1700s – Early 1800s)

Associated with David Ricardo and Jean-Baptiste Say.

Core idea: Markets naturally tend toward equilibrium. Recessions are usually temporary and caused by external shocks or rigidities.

Key belief: Supply creates its own demand (“Say’s Law”).

Central mechanism: External shock → temporary disequilibrium → market adjustment → recovery

Crisis: Temporary disruption caused by external events, price rigidities, or production imbalances.

Modern macroeconomics largely moved beyond pure classical cycle theory after the Great Depression.

2. Marxian Crisis Theory (Mid–Late 1800s)

Associated with Karl Marx.

Core idea: Capitalism contains internal contradictions that generate recurring crises.

Different Marxian versions emphasize:

falling profit rates,

underconsumption,

overproduction,

class conflict,

financialization.

Central mechanism: Capital accumulation → profit compression / overproduction → crisis → restructuring

Crisis: Systemic crisis emerging from the contradictions of capitalist accumulation itself.

Crises are viewed as structural rather than accidental.

3. Austrian Business Cycle Theory (ABCT) (1910s–1930s)

Associated with Ludwig von Mises and Friedrich Hayek.

Core idea: Artificially low interest rates distort investment decisions.

Boom: Cheap credit encourages excessive long-term investment.

Bust: The economy eventually realizes those investments are unsustainable.

Focus:

malinvestment,

credit distortion,

monetary expansion.

Central mechanism: Artificially low rates → malinvestment → unsustainable boom → liquidation crisis

Crisis: Collapse triggered when distorted investments are revealed as unsustainable.

4. Schumpeterian Innovation Cycles (1910s–1940s)

Associated with Joseph Schumpeter.

Core idea: Capitalism evolves through waves of innovation and “creative destruction.”

New technologies create:

investment booms,

industrial transformation,

disruptive restructuring.

Examples:

railroads,

electricity,

automobiles,

internet,

AI.

Central mechanism: Major innovation → investment surge → structural transformation → displacement/crisis → new cycle

Crisis: Disruption caused by technological displacement and industrial restructuring.

5. Keynesian Business Cycle Theory (1930s)

Associated with John Maynard Keynes.

Core idea: Economies can remain stuck in prolonged underemployment because aggregate demand can collapse.

Causes of recessions:

weak consumption,

falling investment,

pessimistic expectations,

financial panic.

Policy response:

Governments should use:

fiscal spending,

public investment,

and monetary easing.

Central mechanism: Demand collapse → falling output/employment → reduced spending → recession spiral

Crisis: Persistent recession caused by insufficient aggregate demand.

Keynes shifted macroeconomics toward demand management.

6. Debt-Deflation Theory (1930s)

Associated with Irving Fisher.

Core idea: Excess debt creates vulnerability.

When asset prices fall:

debt burdens rise in real terms,

spending collapses,

defaults spread,

deflation worsens recession.

Central mechanism: Excess debt → asset-price decline → deflation → rising real debt burden → collapse

Crisis: Debt liquidation and deflation reinforce each other into systemic contraction.

Very influential in understanding financial crises.

7. Monetarist Theory (1950s–1970s)

Associated with Milton Friedman.

Core idea: Business cycles are heavily driven by changes in the money supply.

Recessions occur when:

monetary contraction,

banking failures,

or poor central-bank policy reduce liquidity.

Central mechanism: Money supply contraction → reduced liquidity/spending → recession

Crisis: Severe downturn caused by collapse or mismanagement of money supply.

Friedman argued the Great Depression became catastrophic largely because the Federal Reserve allowed money supply collapse.

8. Financial Instability Hypothesis (1960s–1980s)

Associated with Hyman Minsky.

Core idea: Stability itself creates instability.

During long stable periods:

firms and households take more debt,

speculation increases,

leverage rises,

fragility accumulates.

Eventually:

a shock triggers crisis,

deleveraging causes collapse.

Famous phrase: “Stability is destabilizing.”

Central mechanism: Stability → rising leverage/speculation → fragility → financial crisis

Crisis: Financial panic triggered by excessive leverage and speculative financing structures.

Minsky became extremely influential after 2008.

9. Political Business Cycle Theory (1970s)

Associated with William Nordhaus.

Core idea: Governments manipulate economic policy around elections.

Examples:

pre-election stimulus,

lower interest rates,

tax cuts,

increased spending.

Then inflation or austerity follows later.

Central mechanism: Electoral incentives → expansionary policy → temporary boom → post-election correction

Crisis: Inflationary or recessionary correction following politically motivated stimulus.

10. Real Business Cycle Theory (RBC) (1970s–1980s)

Associated with Robert Lucas Jr., Edward Prescott, and Finn Kydland.

Core idea: Business cycles are driven mainly by real shocks:

technology,

productivity,

energy,

regulation,

resource changes.

Recessions: Not necessarily “failures,” but rational responses to changing conditions.

Central mechanism: Technology/productivity shock → rational adjustment in labor and production → cycle

Crisis: Economic slowdown caused by negative productivity or technology shocks.

RBC heavily influenced modern DSGE macroeconomics.

11. New Keynesian Theory (1980s–1990s)

Modern synthesis combining:

Keynesian demand concerns,

rational expectations,

microfoundations.

Associated economists:

Gregory Mankiw

Stanley Fischer

Olivier Blanchard

Core idea: Markets do not instantly adjust because of:

sticky prices,

sticky wages,

imperfect competition.

Demand shocks therefore create real recessions.

Central mechanism: Demand shock + sticky prices/wages → prolonged output and employment decline

Crisis: Persistent downturn caused by insufficient demand and slow market adjustment.

This became dominant in central banking.

12. Distribution–Leverage Cycle (DLC) (2020s)

Associated with Jo M. Sekimonyo.

Core idea: Structural distributional imbalance forces increasing leverage expansion to sustain aggregate demand and participation. The system appears stable temporarily because debt compensates for weak distributed purchasing power. Instability emerges endogenously as leverage accumulates faster than productive distribution.

Central mechanism: Distribution gap → leverage expansion → temporary stability → debt saturation → instability

Crisis: Systemic instability caused by debt-dependent participation replacing sustainable distributed purchasing power.